I’ve been freelancing as a book cover designer and illustrator since 2019, and saying I had a lot to learn when I left my in-house role after eight years is like saying the Titanic had a bit of a leak. I was absolutely not prepared. No one sat me down to say, “Hey Mic, here’s how to register for VAT,” or even, “By the way, do you actually know what VAT is?” (Spoiler: I did not.)

And contracts? Oh, I should actually read them? Turns out, yes. Yes, I should. Because learning the hard way meant experiencing fun little surprises like when a client disappeared with final files without paying or when I unknowingly agreed to a deal that left me severely underpaid for work that went on to be sold worldwide.

It’s amazing and shocking really that still to this day a lot of universities don’t teach a fundamentals in business on creative courses when such a high percentage of creatives end up freelancing.

That’s part of the reason I’m putting together Fr££lance: How to (and how not to) approach the business side of freelance on May 1st (https://sbf.org.uk/whats-on/view/frlance/) alongside Becky Chilcott, David Pearson, and Jack Smyth. It all started when I emailed Becky one day to ask, “Do people actually care about this stuff?” The answer was a resounding YES. So here we are, creating an evening where we lay it all out on the table: contracts, fees, getting paid what you’re worth, and all the things I wish someone had told me before I jumped into freelancing headfirst.

So give you a little taster before our event I thought I’d share with you 5 things that one should always think about when going freelance.

- The Contract Check List

- Sole Trader or LTD business?

- What is VAT?

- Save your Tax!

- Keeping Track…

1. The Contract Check List:

We’ve all been guilty of skimming a contract and signing on the dotted line, thinking, Eh, it’ll be fine. Until it’s not. Early in my career, I learned the hard way that not all contracts are created equal; some sneak in terms that require more compensation, better clarity, or just a plain hard no. So, before you grab that pen (or digital signature), here’s what to check:

✔ Scope of Work

What exactly are they paying you for? Make sure the fee matches the workload. Are you just designing, or are they expecting the full works—design, illustration and/or art direction.

- Design

- Design and Illustration

- Art Direction

- Illustration only

✔ Territories

Where will your work be used? The broader the rights, the higher the fee should be. If they’re asking for World Rights, that means you won’t get extra sell-on fees if other markets (Europe, America, Mars) want your work later.

- UK/Commonwealth or Single a specific territory

- World English

- World All Languages

✔ Usage & Licensing

How will your work be used? If it’s just for the hardcover, great. But are they also asking for paperback, ebooks, audiobooks, marketing materials, merch, and limited-edition book-shaped scented candles?

- Hardback only or all formats?

- Intended usage outside of the book (i.e. Marketing )

✔ Kill Fees

Is there an agreed term on what are the percentages of the fee you will get if the project gets killed. What are those percentages?

- Terms and percentages

✔ Intellectual Property (IP) Rights

Ensure that the contract explicitly outlines who owns the final design and what rights you (the designer) retain. Are you transferring all rights to the client, or do you retain ownership of the work? Understand whether the work is exclusive or non-exclusive.

✔ Credit & Acknowledgment

How will you be credited on the piece of work? Where will it appear?

✔ Dispute Resolution

It’s also worth checking if the contract includes a clause about how disputes will be handled (e.g., via arbitration, mediation, etc.), which can be crucial if things go wrong.

✔ Sneaky Additional Terms

Some cheeky areas that can creep into contracts can be things like:

- The rights to your unused concepts

- Lack of agreed revisions

- Low/no kill fees

- Full buyout or taking away your rights

- I once got a contract that the usage of my work may include “unknown future uses.” Which was a laughable “no”.

Making sure you check out for all of these things can really give you better footing when agreeing on a fee and making sure that your rights are protected.

2. Sole Trader or LTD Business?

Ah! Now this one was something I had to learn on my own. I had heard whispers about the pros and cons of going Limited, but I never understood what the debate was for both. So here’s a little breakdown to help you gain a better understanding. The main differences between being a sole trader and operating as a limited company in the UK come down to liability, taxation, and administrative requirements.

1. Legal & Financial Liability

Sole Trader: You and your business are legally the same entity. You are personally liable for any debts the business incurs.

Limited Company: The business is a separate legal entity. Your personal finances are protected, meaning you’re only liable up to the amount you invest in the company.

Please note: In any case you should ALWAYS have a separate bank account whether you are a sole trader or operating as a business (more on this later).

2. Taxation

Sole Trader: You pay Income Tax and National Insurance on your profits through Self Assessment. You may also need to register for VAT if your turnover exceeds £90,000.

Limited Company: The company pays Corporation Tax. You, as a director, can take a salary and dividends, which can be more tax-efficient. As a Limited Company you might also have more tax-deductible expenses than a sole trader.

3. Administrative

Sole Trader: Easier to set up and run. You just need to register with HMRC for Self Assessment.

Limited Company: More paperwork, including filing annual accounts, confirmation statements, and tax returns with Companies House and HMRC.

4. Taking Money Out of the Business

Sole Trader: All profits belong to you, but they are taxed as personal income.

Limited Company: Money belongs to the company. You can pay yourself a salary (subject to PAYE) and dividends (which are taxed at lower rates).

5. Costs

Sole Trader: Minimal costs (usually just accounting and tax-related).

Limited Company: Higher costs, including potential accounting fees, Companies House fees, and compliance costs.

So here’s an easier breakdown between the two:

💼 Sole Trader (Best for Beginners & Simplicity)

✔ Quick & easy setup

✔ Fewer admin & accounting costs

✔ Profits taxed as personal income

❌ Unlimited personal liability (your assets at risk)

❌ Higher tax rates once earning over £50k

🏢 Limited Company (Best for Growth & Tax Efficiency)

✔ Lower tax rates (corporation tax + dividends)

✔ Limited liability (personal assets protected)

✔ More flexibility in claiming business expenses

❌ More admin & legal responsibilities

❌ Accountant often required

When to switch?

Earning consistently over £50k → More tax-efficient

Want liability protection → Limited Company shields personal assets

Planning to expand or hire → Easier business structure

3. What is VAT?

Let’s be real, VAT is one of those things that feels unnecessarily complicated. But don’t worry, I’m not here to explain why it exists (because honestly, who really knows?). Instead, let’s focus on the when you need to start adding VAT to your invoices.

In the words taken straight from HMRC: VAT (Value Added Tax) is a tax added to most products and services sold by VAT-registered businesses. Businesses have to register for VAT if their VAT taxable turnover is more than £90,000. They can also choose to register if their turnover is less than £90,000.

So, if you’re making a very healthy £90k+, congratulations! Time to register for VAT. If you’re earning less, you have the option to join the VAT club voluntarily.

Please note: the VAT threshold may change from year to year based on UK government decisions.

Now, here’s a simple breakdown to make it all visually easy to digest:

What is VAT (Value Added Tax)?

- A tax added to goods and services you sell

When to Register

- £90,000+ Turnover? → Register for VAT

- Below £90,000? → Optional Registration

How to Apply

- Apply online with HMRC (or your local tax authority)

- Ask your accountant to do it for you

Consequences of Delay

- Penalties & Interest on unpaid VAT

If you’re anything like me, your next question is, “Once I’m registered, when and to whom do I actually charge VAT on my invoices?” Don’t worry, I’ve got you! Here’s a simple breakdown below.

🇬🇧 UK Customers

- Businesses: Charge VAT unless exempt

- Sole Trader: Charge VAT at 20%

🇪🇺 EU Customers

- Businesses: If your EU client is a VAT-registered business, you do not charge UK VAT. Instead, they handle VAT on their end under the reverse charge mechanism (they report both the output and input VAT on their local VAT return). But note that you must include their VAT number on your invoice.

- Sole Trader: If your EU client is a private individual (not VAT-registered), you must charge UK VAT (20%) if you are VAT-registered. If you are not VAT-registered, you do not charge VAT at all.

🌍 Non-EU Customers

- Generally, no VAT on goods and services

4. Save your Tax!

Now this is something that is so basic but has caught A LOT of freelancers I know when it comes to the end of the tax year. It’s not just about saving the right amount for tax each time you get paid, it’s also about having a little extra set aside. HMRC loves to ask for an advance for the following tax year, so it’s best to be prepared.

The key is to save the correct percentage based on your earnings, plus a little extra as a buffer. Below, you’ll find the latest UK tax rates (and just a heads up, Scotland has different tax bands).

*Taken from www.gov.uk

Please note: that personal allowance of £12,570 is gradually reduced for higher earners (earning over £100,000)

5. Keeping Track…

This is something I wish I created a good system on how to keep track of all my work projects, my expenses, my invoices and my payments before I went freelance. These are some amazing systems that really help me keep track of everything:

Track your work

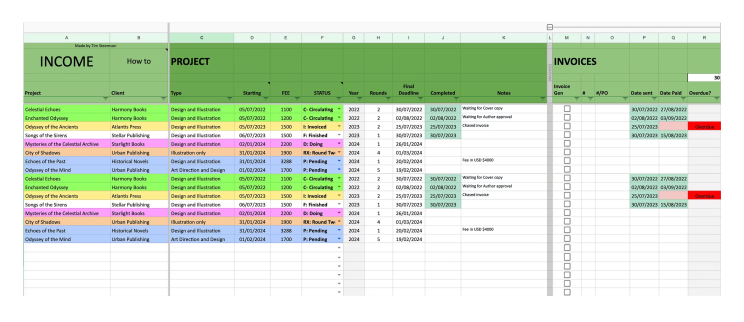

Is it wizardry? Nope, it’s just a super spreadsheet! If you love spreadsheets (or know someone who can create an awesome work tracker for you), this can be a total lifesaver, whether you’re a freelancer or an in-house designer (and definitely ditch those post-it notes!).

I use a Google spreadsheet that’s always online, so I can access it from anywhere. Everything’s colour-coded (because why not?) to help me stay on top of what’s urgent, what I’ve invoiced, and which payments need chasing. Plus, I’ve set it up so that if an invoice is over 30 days old, an automatic “OVERDUE” reminder pops up, keeping me on track with follow-ups. Here’s a sneak peek of my spreadsheet below!

© Tim Steemson

Track your payments

Having a separate business bank account (away from your personal one) will make your life so much easier, especially when tax time rolls around. Keep all your payments and business expenses in this account to stay organised. Personally, I’ve found Wise Bank super helpful (not sponsored, just a fan). They offer low, transparent fees and use real exchange rates, which saves you money on international transfers. Plus, you can hold and manage multiple currencies, so it’s easy to receive payments from clients all over the world without high conversion fees. Since I work with clients everywhere, I can set up different currency accounts under one bank, which means I get paid in the local currency.

Track your invoices and expenses

Aside from using my spreadsheet to keep track of everything, I decided to take it a step further when I became a Limited Company and started using a program called FreeAgent (and no, I’m not getting paid to promote this either!). FreeAgent is awesome for freelancers because it makes accounting so much easier. You can link it to your bank account, so it automatically tracks your income, expenses (you can upload receipts for everything, keeping everything in one place), and invoices (it stores all your client payments and you can upload your invoices to keep them in one place). It also helps with taxes, saving you time and reducing mistakes. Plus, it generates simple end-of-year tax reports, making it super easy to file your tax returns and stay on top of HMRC requirements. And if numbers aren’t your thing, like me, you can share FreeAgent with your accountant so they can access all the info directly from the program.

*Please note that FreeAgent charges to use their program.

In conclusion, navigating the business side of freelancing doesn’t need to be as intimidating as it might seem at first. Sure, there are a lot of moving parts, and learning the hard way can sometimes feel like you’re walking through a maze blindfolded. But with a little preparation, the right mindset, and a willingness to ask the tough questions (no matter how basic they may seem), you can set yourself up for success.

Freelancing is a rewarding journey, but it’s about more than just creating great work. Understanding the contracts, taxes, and business structure behind the scenes is what truly allows you to thrive. Whether you’re a newbie like I was, or a seasoned pro looking to refine your approach, the goal is simple: Get your business side as solid as your creative side.

And if you want to learn more, please join us on May 1st 2025 in-person or online for Fr££lance: How to (and how not to) approach the business side of freelance at St Brides Foundation (https://sbf.org.uk/whats-on/view/frlance/) Tickets still available!

Mentioned resources below :

HMRC – www.gov.uk

Wise Bank – wise.com

FreeAgent – freeagent.com

Please note: that costs and percentages change year to year so please keep up to date each Tax year at HMRC for the latest information.

Micaela’s article was originally published on LinkedIn on April 4, 2025